Despite lingering high inflation, fears of recession, geopolitical concerns and ongoing stock market volatility, Americans continue to be incredibly generous when it comes to charitable giving. In 2021 Americans gave $484.85 billion to various non-profit entities, with nearly $327 billion of that total coming directly from individuals.[i] Americans have demonstrated that even in an uncertain economic environment, they truly want to have a meaningful impact on their communities and around the world.

The reasons for charitable giving vary by individual, with “making a difference” nearly always at the top of the list. However, there are also many incredible tax, financial and family benefits to be considered when making charitable donations. There are many types of charitable giving vehicles, each with their own unique features and benefits. With proper planning in selecting the right one, donors may be able to maximize their tax benefits while accomplishing the goal of helping others.

When making a significant gift to charity, what and how a gift is made can be just as important as where that gift ends up. Identifying the best types of assets to give is the first key to maximizing the tax and financial benefits to the donor. These asset classes can be broken down into two categories – cash and appreciated assets. It’s important to distinguish between these two types as they are treated differently for income tax deduction purposes.

Gifts of Cash: Checkbook philanthropy is the simplest and most common type of charitable giving. Donors can make one-time or recurring donations to a charity using cash, checks, or credit cards. The annual charitable deduction limitation for all gifts of cash is 60% of Adjusted Gross Income (AGI). Charitable contributions in excess of the annual deduction limit may be carried forward for five subsequent tax years as needed.

Gifts of Appreciated Assets: Gifts of appreciated assets such as stocks, mutual funds, closely held business interests, gifts of real property or real estate receive additional benefits over cash gifts. In most cases donations of appreciated assets result in an income tax deduction based on the fair market value of the asset and permit the donor to bypass any capital gains tax that would have been incurred if the asset had been sold and a subsequent cash gift were made. That typically leaves more available resources and increases the power and reach of their charitable gift.

The annual charitable deduction limitation for gifts of appreciated assets is 30% of AGI. Charitable contributions in excess of the annual deduction limit may be carried forward for five subsequent tax years as needed. It is important to remember that any donation of over $5,000 in value requires an appraisal, unless it is a gift of publicly traded stocks, bonds, or mutual funds.

Once the asset type has been identified, there are many different charitable giving vehicles that can be used based on the donor’s goals and specific circumstances. Selecting the appropriate vehicle can greatly increase the impact and efficacy of the gift for both the receiving charitable organization and the donor. Here is a breakdown of the various options available.

Private Foundations: Private foundations play an important role in helping fund charitable activities around the world. Some types of private foundations have the ability to execute their own charitable programs. For the most part, however, private foundations are organized for the purpose of financially assisting qualified public charities through grants. Families enjoy the amount of flexibility and control that their private foundations offer. Control of the foundation (via the Board of Directors) can be held by related parties, family members or other closely connected individuals.

Private foundations can be funded with all types of appreciated assets, although there are some additional limitations to cost basis deductions for contributions made with assets other than cash and publicly traded securities. Investments held by a foundation can grow in a tax-preferred environment while a minimum of 5% of net assets must be used for grants and charitable purposes annually. These foundations are intended to be endowments earmarked for the benefit of charitable organizations and efforts, thus affording families the opportunity to include children and grandchildren in their philanthropic vision and legacy. Close family board control can ensure ongoing charitable family involvement for generations to come.

Although private foundations are incredibly flexible, they are also subject to much tighter IRS compliance scrutiny and regulations than public charities. It is strongly recommended to engage a third-party administrator to ensure that these foundations stay in compliance with current filings and regulations.

Donor-Advised Funds (DAF): DAF’s have become the most popular gifting vehicle in recent years as they offer many ongoing benefits and long-term involvement for donors with less administration and regulation than a private foundation. A DAF’s purpose is to financially support qualified charitable organizations over time through annual grants to public charities.

Unlike private foundations, DAF’s are not required to independently incorporate or register with the IRS. DAF’s are charitable giving accounts established at a sponsoring, qualified 501(c)(3) public charity. These accounts are segregated, for accounting purposes, to give donors the look and feel similar to a private foundation without the heavy administrative burden. Once the DAF is funded, grants are recommended by the donors and are made directly from the sponsoring charity. Acknowledgement of the donors recommending the grant (or DAF name) is typically included with the grant. The accounting and any required filings are provided by the sponsoring charitable organization, thus reducing the amount of cost and time to administer the account.

Similar to private foundations, contributions to a DAF may be made with cash, publicly traded stock, real estate, and many other types of appreciated assets. Assets contributed to a DAF generally create an immediate income tax deduction for the donor, may potentially bypass capital gains tax, remove taxable assets from a donor’s estate, and may be invested tax-free. For income tax purposes, contributions to a DAF are treated as if the donation was made directly to a public charity such as a church or public school. In contrast to private foundations, an income tax deduction equal to the fair market value of the assets gifted applies to all contributions (even for closely held businesses and other appreciated assets). A DAF is intended to be an ongoing, endowed family charitable legacy for generations to come. The process to establish and use a DAF is very simple:

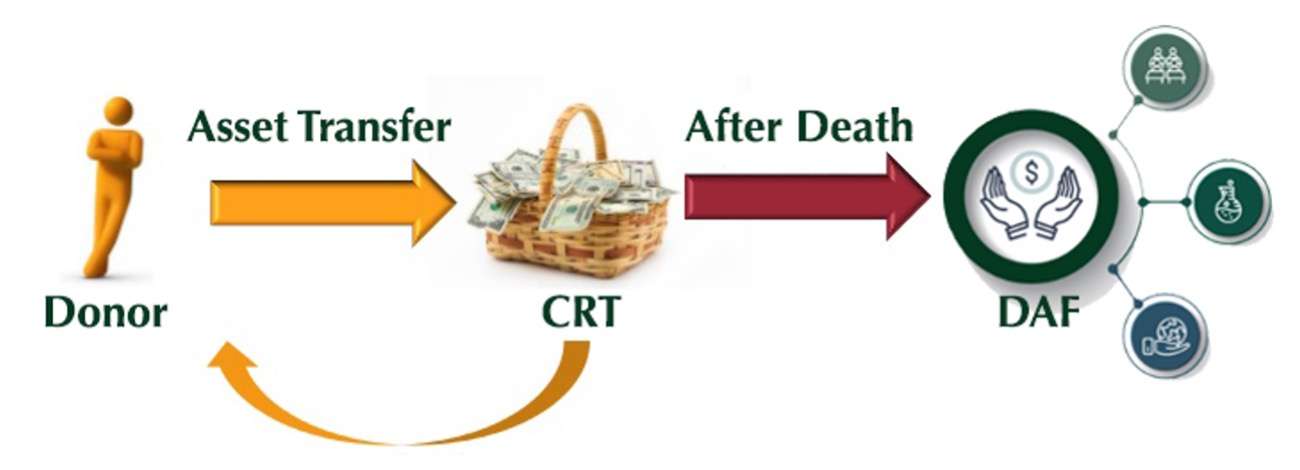

Charitable Remainder Trusts (CRT): A CRT is an irrevocable trust that is designed to provide an income stream for the donor and his or her spouse, or even to other beneficiaries for a term of years or for the donor’s lifetime. After the term of years or upon death, the remainder of the trust transfers to the donor’s favorite charity or to his or her own private foundation or DAF. A CRT can provide the following benefits:

- Income for the donor and his or her spouse during their lifetime(s)[ii]

- Can be funded with appreciated assets

- Receive a partial income tax deduction (for the estimated present value of the remainder interest of the gift)

- Bypass capital gains tax

- Bypass estate tax

- Fund your DAF or private foundation after death

Charitable Lead Trusts (CLT): A CLT is an irrevocable trust that works inversely to a charitable remainder trust. Instead of providing an income stream to the beneficiaries, a CLT provides an income stream to one or more charities, or to a DAF or private foundation, for a term of years. The remaining assets transfer to family members or other beneficiaries at the end of the trust term. CLT’s can provide the following benefits:

- Income tax deductions (for the estimated present value of the income payments made to the charity)

- Gift tax savings on transferred assets

- Bypass state tax

- Fund a DAF or foundation now instead of after death

Volunteering Time and Services: Donors can also give their time and skills to charities as this is an essential part of charitable giving. This can include anything from volunteering at a soup kitchen to tutoring students. An estimated 23.2 percent of Americans (more than 60.7 million people) formally volunteered with organizations between September 2020 and 2021. In total, these volunteers served an estimated 4.1 billion hours with an economic value of $122.9 billion.[iii] Even with numbers skewed over the pandemic, the trend of volunteerism continues to grow year over year. Volunteering not only makes a difference now with actual boots on the ground, but it can also be a very effective way to assess needs to formulate future gifts to charitable organizations.

Each type of charitable giving vehicle has its own advantages and limitations. Each donor has different circumstances, goals, and objectives. Knowing the landscape of charitable giving will better help you to find the best fit for your next planned charitable gift. To design the perfect gift, it is always important to consult with your financial advisor and tax professional to determine which charitable giving vehicle is best for your specific situation. At Crewe Foundation, we work with your trusted advisors and bring decades of advanced gift planning experience to help you design and implement your next charitable gift.

[i] Giving USA 2021 Annual Report

[ii] Distributions to beneficiaries may result in income tax liability

[iii] AmeriCorps, Office of Research and Evaluation