Introduction

Corporate Executives typically receive a significant portion of their compensation in the form of equity. This equity compensation can take many forms, each with its own features, risks, benefits, requirements, and tax implications. It is critical for executives and their advisors to understand the structure of their particular equity compensation so they can make the best planning decisions and seek to minimize tax impacts. Some of the more common forms of equity compensation include:

Stock Options

A stock “option” is the right (not the obligation) to purchase shares at a specified exercise price at some future point(s) in time. A major benefit to employees granted options is that, at the time of exercise, there may be a significant difference in the price paid (exercise price) to acquire the shares and the current market value of those shares. The difference between the exercise price and the market value at the time of exercise is termed the “bargain element” (an important concept for tax planning that will be discussed later). For instance, if an employee was granted options to purchase 500 shares of stock at $10/share and the stock at the time of exercise was trading at $50/share, the bargain element would be $40/share.

While often just referred to as “options” generally, there are actually multiple types of options to become familiar with. We will discuss two common types here, Incentive (also called Qualified) Stock Options or ISOs and Non-Statutory (also called Non-Qualified) Stock Options or NSOs. Incentive Stock Options (ISOs) are stock options that meet statutory requirements for preferential tax treatment. NSOs are stock options that do NOT meet the statutory requirements for ISO taxation and therefore do not enjoy the same potential tax advantages. This distinction is important when creating an exercise strategy.

In the case of ISOs, no tax is due on the previously discussed bargain element in the year of exercise (however, the amount of the bargain element is included for the Alternative Minimum Tax (AMT) calculation). If the shares are then sold (at least 2 years after the grant date and 1 year after exercise), all capital gains will be treated as long-term in nature. This can be advantageous to the taxpayer as long-term capital gains rates are lower than ordinary income rates.

On the other hand, NSOs do not qualify for this tax treatment and the bargain element is taxable as ordinary income in the year of exercise. In the example above, this could result in the bargain element of the NSOs being taxed at the maximum federal tax rate (including the 3.8% Medicare surtax) of 40.8%.

The timing of when to exercise NSOs should be examined carefully to achieve the most optimal outcome. For example, if the holder of the NSOs anticipates being in a lower tax bracket in certain years, it may make sense to time the exercise of options in those years as opposed to higher-tax years. It may also make sense to exercise NSOs if it is anticipated that the stock will appreciate rapidly and/or significantly. Continuing the previous example, if the stock grew from $50/share to $100/share after exercise, then exercising when the stock was at $50 would have resulted in $40/share being taxable at ordinary income rates and the remaining $50/share of gain (if held for 1-year post-exercise) being subject to long-term capital gains treatment. Contrast this with waiting to exercise until the stock price was already at $100/share. At this point, the entire $90/share in gains would all be subject to ordinary income tax rates.

Eligible

Employees Only

Employees &

Non-Employees

$100k

None

Taxation at Issuance (Grant)

None

None

Taxation at Exercise

No tax on bargain element, but it is an Alternative Minimum Tax (AMT) preference item

Bargain element taxable as ordinary income in year of exercise

Taxation Upon Sale

Long-term capital gains tax treatment if holding period requirements are met

Gain after exercise taxed at capital gains rates

Holding Period for Favorable Tax Treatment

Held for 2 years after grant and 1 year after exercise; also, must still be an employee within 90 days of selling

N/A

Eligible

Employees Only

Employees &

Non-Employees

$100k

None

Taxation at Issuance (Grant)

None

None

Taxation at Exercise

No tax on bargain element, but it is an Alternative Minimum Tax (AMT) preference item

Bargain element taxable as ordinary income in year of exercise

Taxation Upon Sale

Long-term capital gains tax treatment if holding period requirements are met

Gain after exercise taxed at capital gains rates

Holding Period for Favorable Tax Treatment

Held for 2 years after grant and 1 year after exercise; also, must still be an employee within 90 days of selling

N/A

Restricted Stock & Restricted Stock Units (RSUs)

The terms restricted stock and restricted stock units (RSUs) are often used interchangeably but are different in application. Employees granted shares of restricted stock are granted actual shares of company stock subject to some restriction(s) such as a vesting schedule. At the end of the vesting period and/or other restrictions the shares become the employees. In contrast, RSUs represent an unsecured promise by the company (not actual shares) to grant shares at a future date. As with restricted stock, RSUs are typically subject to a vesting schedule. Once the vesting period has been met, stock or cash is delivered to the employee. With both restricted stock and RSUs, the value of the shares is taxable as ordinary income in the year of vesting.

One key difference between restricted stock and restricted stock units is the availability of the 83(b) election. Making an 83(b) election allows the recipient of restricted stock to voluntarily elect to recognize tax on the shares in the year they are granted as opposed to the year they vest. Any gain above the grant price would then potentially be eligible for taxation at long-term capital gains rates instead of ordinary income rates. This could be advantageous if the shares appreciate significantly between the grant date and vesting as a smaller amount of the value received would be subject to ordinary income taxation. RSUs, on the other hand, are not eligible for 83(b) election because actual shares are not granted on the grant date.

Regarding 83(b) election, it is important to remember that this election does come with certain risks. First, the election is irrevocable and carries with it the risk that the recipient could pay tax on shares that they never actually receive. There is also a risk that the recipient will pay more in taxes than necessary due to a falling share price and/or lower marginal tax rates in the future. Finally, there is an opportunity cost equal to the rate of return foregone on the money used to pre-pay the tax at grant.

Restricted Stock

Restricted Stock Units (RSUs)

An unsecured promise by the company (not actual shares) to grant shares at vesting

Taxation

Restricted Stock

Ordinary income on value at vesting (unless 83(b) election is made); capital gains on growth thereafter

Restricted Stock Units (RSUs)

Ordinary income on value at vesting; capital gains on growth thereafter

Section 83(b) Eligible

Restricted Stock

Yes

Restricted Stock Units (RSUs)

No

Settlement

Restricted Stock

Must be in stock

Restricted Stock Units (RSUs)

May be in stock or cash

Restricted Stock

Restricted Stock Units (RSUs)

An unsecured promise by the company (not actual shares) to grant shares at vesting

Taxation

Ordinary income on value at vesting (unless 83(b) election is made); capital gains on growth thereafter

Ordinary income on value at vesting; capital gains on growth thereafter

Section 83(b) Eligible

Yes

No

Settlement

Must be in stock

May be in stock or cash

Phantom Stock & Stock Appreciation Rights (SARs)

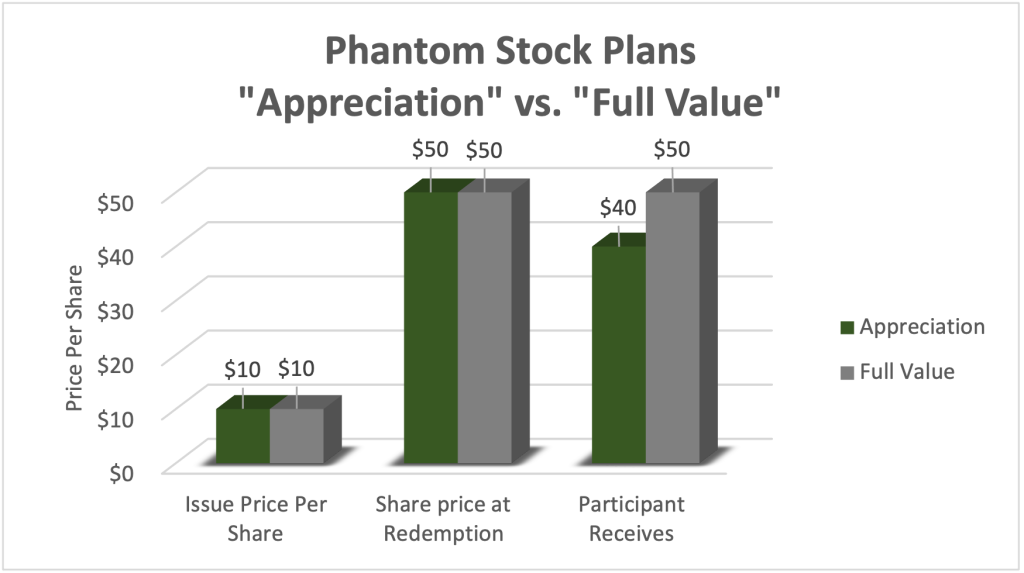

Phantom stock plans are deferred compensation plans designed to give certain employees the opportunity to participate in the upside of company stock. As opposed to receiving actual shares, plan participants are given “phantom” shares (a contractual agreement between the company and participants) that track the performance of the underlying company shares. These phantom shares can be designed to track just the appreciation of underlying shares or to track the full value of the underlying shares.

Phantom Stock

Issue Price Per Share

Appreciation

Full Value

$10

$10

Share price at Redemption

Appreciation

Full Value

$50

$50

Participant Receives

Appreciation

Full Value

$40

$50

Phantom Stock

Full Value

Issue Price Per Share

$10

$10

Share price at Redemption

$50

$50

Participant Receives

$40

$50

The cash value of the Phantom stock benefit is taxable at ordinary income rates in the year it is received.

Additionally, phantom stock can include the value of dividends and stock splits.

Stock appreciation rights (SARs) give recipients the opportunity to participate in the future appreciation of company stock. They are subject to a vesting schedule as well as an expiration date. The expiration date presents a risk to participants as it is possible for the award to expire worthless. Below is an example of the calculation of value of SARs.

“Shares” Granted

1,000

$10

Exercise Price

$15

Price per Share at Exercise

$25

Value Received per Share at Exercise (Price per Share – Exercise Price)

$10

Total Value Received at Exercise

(Taxed at ordinary income rates)

$10,000

Determining the optimal strategy for equity compensation is a multidisciplinary exercise and can be complex. Therefore, it is imperative that clients surround themselves with a team of experts in different disciplines (financial, tax, legal, etc.) to ensure that the chosen strategy aligns with their personal circumstances and desired outcomes.

Crewe Advisors is not an accounting firm and does not provide accounting advice. You should always consult with your tax professional regarding any tax matter.